(Bloomberg) -- Hong Kong stocks headed for their worst loss since the global financial crisis after Beijing announced its intention to impose a national security law on the city, which could trigger a new round of protests as well as heighten tensions with the U.S.

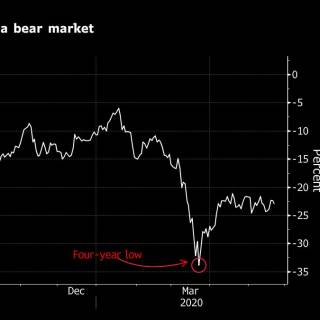

The MSCI Hong Kong Index fell 6.8% on Friday, which would be its biggest slump on a closing basis since October 2008. Real estate firms were the worst hit amid concern over potential outflows and curbed spending, with Sino Land Co. and Link REIT plunging the most since 2008. The Hang Seng Index sank 5.6%, while the Hong Kong dollar weakened to a six-week low.

Concern over the scope of the measures, which would target secession, sedition, foreign interference and terrorism, threatens to end the relative calm that’s endured in the city of 7.5 million since the coronavirus outbreak was reported in January. The uncertainty may also spur residents and investors to park their money outside the city, a trend that was seen last year.

“We could have new protests,” said Kenny Wen, strategist at Everbright Sun Hung Kai Co. Ltd. “Local tensions could trigger Sino-U.S. tensions and the latter is much more stressful for market sentiment and the macro economy.”

China will improve national security in Hong Kong, Premier Li Keqiang said, a day after China announced dramatic plans to rein in dissent by writing a new law into the city’s charter. The law was expected to pass China’s rubber-stamp parliament -- delayed from March by the coronavirus outbreak -- before the end of its annual session May 28.

Sino Land, Link REIT, Wharf Real Estate Investment Co. and New World Development Co. plunged more than 9%. The city’s pegged currency, which had been near the strongest it can trade versus the greenback since late March due to relatively tight liquidity, weakened to 7.7568.

U.S. President Donald Trump said Thursday that the U.S. will “address very strongly” any Hong Kong crackdown. Two U.S. senators also proposed a bipartisan bill that would sanction enforcers of the proposed law. Secretary of State Michael Pompeo has delayed an annual report on whether Hong Kong still enjoys a “high degree of autonomy” from Beijing, telling reporters this week that he was “closely watching what’s going on there.”

Hong Kong’s economy has struggled under the double blow of anti-government protests and the virus epidemic, with the latter prompting the shuttering of borders to non-residents. Gross domestic product contracted by a record 8.9% in the first quarter from a year ago, and the unemployment rate has risen to the highest since 2009. One in four retailers could disappear by December if sales don’t improve, according to an industry association.

Activists were already calling for protests against the legislation China introduced Friday. But social distancing laws still restrict gatherings to no more than eight people, making a return to the massive protests of 2019 hard to achieve for now. The current rules were recently extended to June 4, when tens of thousands typically gather to mark the military crushing of the 1989 protests in Beijing.

Outflows may also pose a significant threat to the global financial center. The Bank of England said in a financial stability report last year that protests led to billions of dollars being pulled from investment funds in Hong Kong, an assessment disputed by the Hong Kong Monetary Authority.

“Investors, especially foreign funds, will be cautious about parking their money in the Hong Kong market,” said Ronald Wan, chief executive officer of Partners Capital International Ltd.

For more articles like this, please visit us at bloomberg.com

©2020 Bloomberg L.P.