(Bloomberg) -- China has driven borrowing costs to multi-year lows as part of efforts to support the nation’s economy. That’s having an unwelcome side-effect for Beijing.

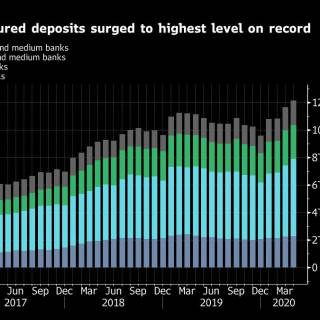

Companies are taking advantage of recent easing measures by the People’s Bank of China, using cheaper funding from bank loans and proceeds from selling bonds to purchase so-called structured deposits offering generous yields. Demand is surging, with the outstanding amount of the products jumping by 2.5 trillion yuan ($350 billion) this year to hit a record high in April.

It has caught the attention of authorities. Premier Li Keqiang last week called for tighter rules to prevent funds circulating back into the financial sector, while Everbright Bank Co. was recently fined over its role in selling some products. The trade means cheaper funding ends up back in the financial sector instead of being used by companies to expand their businesses and support an economy growing at the slowest pace in decades.

Banks offering the products are at risk because they will be left paying structured deposits’ yields in a world of declining interest rates, according to Ming Ming, head of fixed-income research at Citic Securities Co., China’s biggest brokerage.

“It’s a short-sighted move by commercial banks,” he said. “It’s going against the regulators’ will, and it will pressure lenders’ profitability.”

The outstanding volume of structured deposits stood at 12 trillion yuan last month, according to official data. The bulk of this year’s rise is accounted for by companies’ savings at small and medium banks, which surged 1.5 trillion yuan in the last four months, the data showed. The boom follows Beijing’s moves to ease monetary policy, which sent the one-year corporate bond yield to a decade-low of about 1.8% and an interbank rate to 1.3% last month.

Meanwhile, yields on structured deposits of the same tenor are about 3.4% to 4%, according to Everbright Securities Co. That makes it lucrative for investors to use bond proceeds to buy the products, which invest in everything from gold to oil options.

The rising popularity of structured deposits contrasts with the decline of wealth-management products, the shadow-banking vehicles at the center of a regulatory crackdown since 2017. Some investors have shifted their funds into structured deposits from WMPs, most of which no longer guarantee returns, said Harry Hu, senior director for financial institutions ratings at Standard & Poor’s Hong Kong Ltd.

Beijing’s efforts to cool growth in the business have yet to pay off. The PBOC has issued three statements and guidelines to tighten regulations on structured deposits since September. Earlier this month, China’s banking and insurance watchdog fined a branch of Everbright Bank Co. for helping a client use loans obtained from the lender to buy the product.

“It’s very difficult to root out the practice when demand in the real economy is so weak,” said Shujin Chen, a China banking analyst with Jefferies Group LLC in Hong Kong. “What China needs to do is to use fiscal stimulus and boost demand, otherwise structured deposits will be popular due to the loose liquidity.”

Authorities are already trying to do just that. China has expanded its 2020 budget deficit target to 3.6% of gross domestic product, compared with 2.8% last year. This means the central and local governments will sell more bonds to support infrastructure.

Looking ahead, it’s unlikely structured deposits will keep growing at the recent fast pace, according to Nicholas Zhu, a senior analyst at Moody’s Investors Service (Beijing) Ltd. Regulators will continue to have a tight grip on the industry, for fear that a rapid expansion may threaten financial stability, he added.

“Banks will have to make the painful decision of whether to keep rolling their structured deposits forward amid tighter rules, to seek deposits elsewhere or to shrink their balance sheets,” Zhu said. “Regulators will keep the rules tight, as they don’t want to see unhealthy competition among banks or China’s financial stability being challenged.”

(Adds details on a surge in corporates’ holdings of structured deposits in paragraph below chart.)

For more articles like this, please visit us at bloomberg.com

©2020 Bloomberg L.P.