(Bloomberg) -- Argentina’s bonds jumped to the highest this year after it struck a deal with its top creditors to restructure $65 billion of debt, setting the stage for the South American nation to emerge from its third default since the turn of the century.

The country’s $3 billion of bonds due 2048 climbed more than 3 cents to 47 cents on the dollar, after the government said in a statement Tuesday that the deal with key creditors would provide “significant debt relief” and that interest and capital payment dates for some new exchange bonds were moved forward to reach the agreement. While the statement didn’t provide a net-present value for the pact, creditors have said the deal is worth about 55 cents on the dollar.

The agreement is the product of months of negotiations between the government and large investment firms including BlackRock Inc., Ashmore Group Plc, and Fidelity Investments, and is the first step toward stabilizing a floundering economy. Inflation hovers near 45%, the peso has lost more than half its value in just a few years and gross domestic product is set to shrink for the third consecutive year.

READ MORE: Argentina Ends Months of Negotiations With Debt Deal: Timeline

“We’re making good on our word to put the country back on its feet and that the debt wasn’t going to impede us from achieving a process of development for jobs and production,” Argentina President Alberto Fernandez said Tuesday from the presidential residence. The agreement, which represents $38 billion of relief over 10 years, gives Argentines “the autonomy to decide what country we want.”

Three largest creditor groups said in a joint statement that they were pleased to have reached a deal in principle with the government, and that all creditors should support the agreement. Two of those groups, Argentina’s Exchange Bondholder Group and the Argentina Creditor Committee, reaffirmed their support in separate statements.

The deal is “good for Argentina, it’s good for its 45 million people, and it’s good for its creditors, and ultimately, that’s why logic prevailed at the end of the day,” said Gramercy Funds Management founder Robert Koenigsberger in a Bloomberg TV interview.

Economy Minister Martin Guzman said in a press conference that the country expects “very high” participation from bondholders in the upcoming restructuring, and that the exchange will likely meet the minimum thresholds, known as collective action clauses, needed to push the debt restructuring through.

The country and its creditors had volleyed offers for weeks over teleconferencing app Zoom, Koenigsberger added, discussing the length of the payment delay, changes to the legal language in the bonds’ contracts, how interest on the securities issued in the restructuring would be paid, and the amount of principal haircut -- if any -- to stick investors with.

But the major breakthrough came in an Aug. 2 call between Argentine Economy Minister Martin Guzman and BlackRock Inc managing director Jennifer O’Neil, according to people familiar with the matter. The two sides discussed an agreement where Argentina would receive around 37.7 billion in debt relief over ten years, and bondholders would get a value close to the midpoint of the two most recent offers from creditors and the government.

”We reached an agreement that both sides can live with,” said Graham Stock, senior emerging markets strategist at Bluebay Asset Management, which participated in the talks. “To say they’re happy with it would be an overstatement, but they can live with it and it has been the result of compromise.”

Under terms of the accord with the three bondholder groups -- the Ad Hoc Group of Argentine Bondholders, the Exchange Bondholder Group, the Argentina Creditor Committee -- the country will extend its debt offer invitation until Aug. 24, while the settlement date remains Sept. 4.

Back and Forth

The 54.8 cents on the dollar is well above where most of the country’s debt is trading -- around 45 cents on average -- but represents a painful loss for creditors who rushed to lend a few years back on hopes that then-President Mauricio Macri would spur years of growth.

But Macri wasn’t able to accomplish what he promised, and the investment-led boom failed to materialize as inflation soared and the country was forced to turn to the International Monetary Fund for a record $56 billion bailout. The leftist Alberto Fernandez took over as president in December and began steps to restructure, saying the debt load wasn’t sustainable.

The agreement paves the way for the country and its largest creditors to drum up the support needed to finalize a restructuring. Notes issued in 2005 and 2010 require sign-off from at least 85% of holders of all bonds affected to make changes, versus the two-thirds or 75% threshold on securities issued more recently.

The latest agreement removes the incentives for investors to hold out, Koenigsberger said, adding that he expects the government to meet the minimum thresholds.

“What Argentina 2020 is going to demonstrate is, the holdout saga of 2005 to 2016, that was an outlier,” he said, referencing Argentina’s legal battle with creditors that kept it locked out of international markets for a decade earlier this century.

The deal moves up the payment dates on the new bonds to January and July from March and September, while capital payments begin as early as July 2024. Accrued interest will also pay out in a bond which will mature in 2029, earlier than what the government had previously offered. Argentina also says it will change “certain aspects” of legal terms on the new instruments, known as collective action clauses, in order to “address proposals submitted by members of the creditor community” on the contractual framework, a key snag during the talks.

Argentina’s three main bondholder groups say they represent 60% of bonds outstanding from the country’s previous restructurings -- known as exchange bonds -- and 51% of the outstanding global bonds issued from 2016.

Eyes on the IMF

With the debt deal with bondholders near complete, Fernandez must now turn his attention toward the IMF as the country looks to resolve issues with its senior creditor and replace the failed financing arrangement signed under Macri in 2018.

IMF Director Kristalina Georgieva praised the deal in a tweet, saying that the agreement was an significant step. Economy Minister Guzman said Argentina cancelled the previous standby-arrangment with the Fund, and would seek a new agreement that was “very distinct” from the previous one.

“With a lowered external debt burden for the sovereign, getting IMF funding should in principle be easier than it would otherwise have been,” said Richard Briggs, an emerging-markets debt investment manager at GAM Ltd. in London.

READ MORE: Argentina Debt Agreement Lifts Hopes of Easing Economic Distress

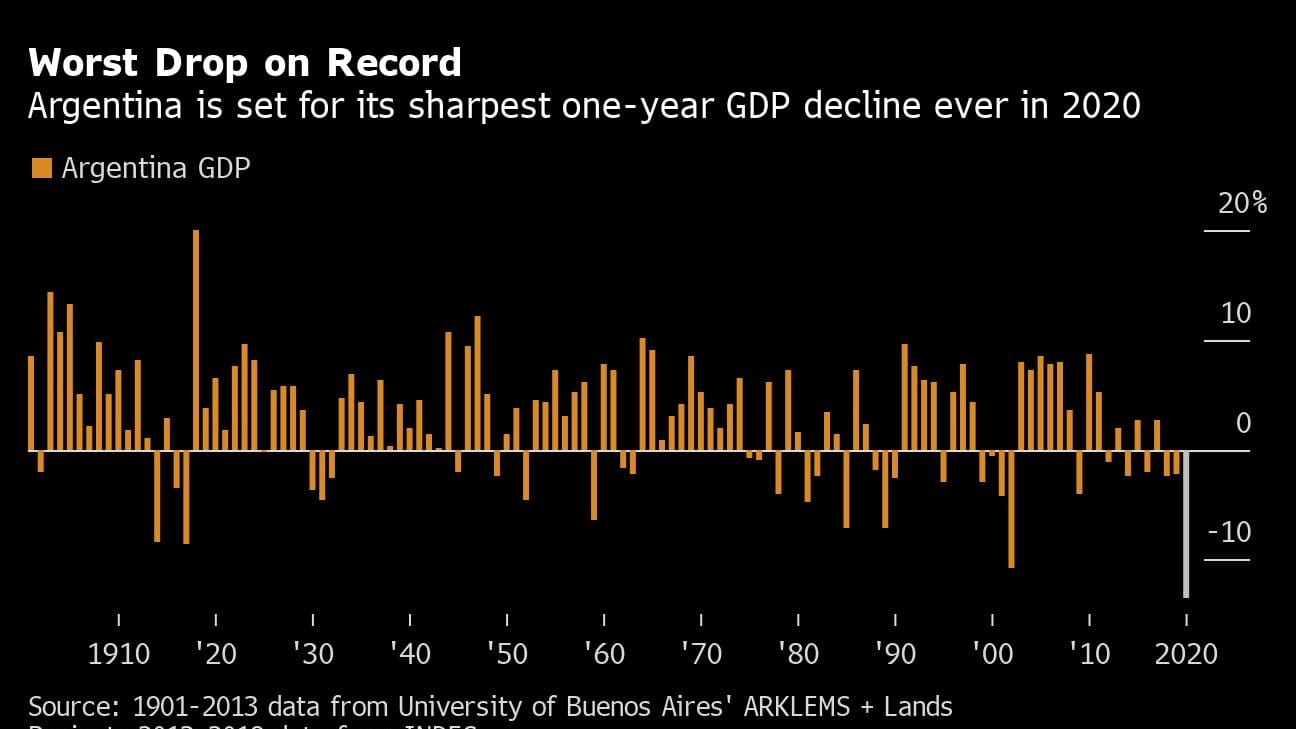

Fernandez must also focus on reigniting an economy that has been shuttered for months, and sparking growth as the country braces for one of its sharpest economic contractions on record. Bank of America analysts are forecasting a 13.5% decline in gross domestic product this year, while Argentina’s central bank economists expect a contraction around 12%.

The country must do this all while continuing to reopen from its strict Covid-19 quarantine, which has been in place since March 20. Despite relatively fewer virus cases in Argentina, the strict lockdown crushed an already-fragile economy while the government has printed money without access to credit, stoking fears of higher inflation to come. Argentina is bleeding precious dollars, even with capital controls in place that keep the peso’s official exchange rate overvalued while the unofficial free exchange rate slides.

READ MORE: In Perennial Economic Crisis, Argentina Faces Worst Year Yet

The central bank has said it could ease capital controls once the debt talks are resolved, and Argentines are bracing for the government to devalue the official exchange rate to encourage exports and bring more dollars into the economy. Argentina’s international reserves hover near a four-year low, totaling less than they did when the IMF program began in 2018. Guzman said in a Bloomberg TV interview July 28 that the country wouldn’t tap international credit markets “for quite awhile.”

The deal also marks the second debt breakthrough for a South American nation in a matter of days. Ecuador on Monday won the support of enough bondholders to restructure $17.4 billion in international debt, almost a third of its total foreign obligations. The country, which received backing from holders of over 95% of its bonds, said it will extend the deadline for creditors to participate in the debt offer until Friday to allow for holders who didn’t vote yet.

Both Argentina and Ecuador’s debt should outperform peers “over the coming days and weeks,” said Paul Greer, a money manager at Fidelity International in London.

(Updates with economy minister’s comments in seventh paragraph and analyst’s comment in tenth paragraph.)

For more articles like this, please visit us at bloomberg.com

©2020 Bloomberg L.P.